Finding out that you have a low credit score can be downright discouraging. Trying to get a personal loan with fair credit may make you feel like it’s not even worth your time and effort. And not being able to borrow money when you desperately need it or want to use it to improve your life, i.e. and a new home for your family, can make you wonder why you even try.

Don’t fret, however. There is hope! Take a deep breath, grab a cup of coffee, and find a comfortable seat. We are going to learn ways to get loans and build our credit. Let’s dive in!

What is a Fair Credit Score?

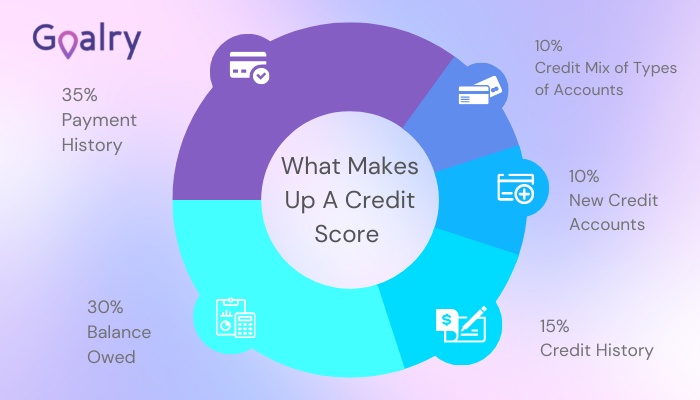

So you have found out that you have a fair credit score. Fair? you think. That can’t be too bad, can it? Before we learn how to fix it and how to use it, let’s first try to understand it. When you apply for a personal loan, your creditworthiness is often judged according to a FICO score. FICO scores range from 300 to 850 and are broken down into the following categories:

- 300 – 579 Very Poor

- 580 – 669 Fair

- 670 – 739 Good

- 740 – 799 Very Good

- 800 – 850 Exceptional

As can be seen, by these categories, fair credit is only one step above very poor credit. This credit standing is considered to be “less than desired” by lenders. About 20% of people have fair credit scores. Though it may be possible to receive a personal loan with a fair credit score, it can often mean less than favorable terms such as higher interest rates. Most lenders, however, will likely reject applicants with this score.

Personal Loans for Fair Credit May Cost More

We said that a fair credit report often means higher interest rates. You have probably heard it before from other sources, too, but do you know how much higher exactly? Let us put it into perspective. A person with fair credit looking for an auto loan will likely pay 311% more interest than one with very good credit. If you are looking for a personal installment loan, you will likely pay around 271% more interest.

That is an extreme difference! The amount you pay in interest could pay for a nice vacation, a new car, or a new house. In fact, CNBC reports that “the person with a lower credit score could pay as much as $45,283 more in borrowing costs than someone with a very good score”.$45,000!! That’s more than some people make in a year! Here is a personal loan calculator to help you understand how to get a loan with fair credit and access to lenders who might be able to help you understand what you can expect to pay.

How Does a Fair Credit Score Affect Your Chances of Getting Approved for a Personal Loans?

With a lower credit score, access to personal installment loans may be limited but not totally out of reach. With some lenders, the score itself is not the biggest factor. Some are more concerned with your income and stability, i.e. the length of time at a residence or job. Others care more about what type of debt is on your credit report. Still, others look to see if your most recent credit factors are positive or negative meaning if the last year you have nothing but positive payment marks, that outweighs some previous bad marks.

The bottom line is that there are many loan options, many lenders, and many loan terms available. With some research and persistence, you will likely find a loan that fits your needs. People usually don’t buy the first car or house you run across. You look around, research, and ask questions about each you are interested in. You then calculate whether or not it fits your budget or if you need to make any changes in order to make that purchase. It is a decision you do not make lightly. Personal loan shopping should be taken as seriously.

How to Bring Your Credit Score From Fair to Good

Before you can improve your credit, you have to know exactly what needs to be improved. Visit AnnualCreditReport.com to get your free annual report from all three credit agencies. Once you receive them, sit down and answer the following questions:

- How much do you owe?

- What will be coming off of your credit report soon?

- What is causing the greatest negative impact?

- Are there any mistakes on the report? (If so, dispute it with the credit bureau.)

- Are there any debts you are aware of that are not on your report yet but will be soon?

Once You Have This Information, You Can Start Making a Plan

Put your debts in order from either smallest to largest (debt snowball) or largest to smallest (debt avalanche). At the top of the list, place the debts that have not reached your report yet. These should be the ones you pay first. It’s hard not to jump straight to debts that are on your report, but paying those debts will not do you any good if negative marks are added at the same time. Once you get those debts paid, you can start working on the things that are on the reports. You can use an app like Debt Payoff Planner to help you track and organize the debts you need to pay.

Another step in building your credit is by adding positive things to your report. You still have a few options for this, even with low credit. Secured credit cards are a great option. Some jewelry stores may allow a small amount of credit. Some people even go to extreme lengths such as taking out a payday loan, paying it right back in a few days, and either asking the company to report your payment or turning the receipts into the credit bureaus. There are options available if you search for them.

The Best Places to Get a Loan When You Have Fair Credit

Even with low credit scores, there are options for getting a loan. Below are three of these options:

✓Banks and Credit Unions

Both banks and credit unions can assist you with getting a loan. However, you may have a better chance and better results with a credit union. Credit unions are not-for-profit organizations. Therefore, they are usually more willing to work with their members and offer lower interest rates. They also usually offer secured loans, which banks normally do not offer. With these loans, the borrower places a certain amount, usually 100% of the loan, into a savings account and the credit union loans them that money. The bank has no risk because they can just take the money from the savings if you do not make the payment.

However, paying benefits the buyer by building credit with the credit union that reports to the credit bureaus. Also, the money that in the savings account usually gains some interest, an added benefit.

✓Peer to Peer Lenders

For the past decade or so, peer to peer lending has been a potential alternative. People can loan money to others through a peer to peer lending platform. Borrowers have another avenue to borrow money and lenders have the opportunity to make money on their investment.

What Other Reasons Determine Your Ability to Get a Loan Besides Credit Score?

As previously stated, your credit score is not the only thing that lenders pay attention to. Other factors may have more weight as to the reasons personal loans are rejected. At the very least, tip the scales a bit (hopefully in your favor). So what are these other reasons? Your income, your debt, and the number of loans and inquiries on your credit report.

This applies to everyone, regardless of your credit score. It does not matter if you have perfect credit if you have no income, or if your income is less than your outgoing. Lenders need to know that you have the ability to pay back the loan. Additionally, they will generally want to see that you have been making this income for a certain period of time (the longer, the better). This helps show stability.

Lenders will look at how much debt you have compared to your income, or your debt to income ratio. If your debt outweighs your income, they will assume (logically so) that you will not have enough money left to pay your loan back. They will also pay attention to how long you have had the debt and whether you are making any payments toward it. Many times, the type of debt you have will be a factor. Hospital bills and student loans generally do not hold the same weight as personal installment loans, credit card debt, auto loans, etc.

Even if your credit is in pretty good shape, if you have too many open loans, lenders generally will not approve your loan request. The same goes if you have too many loan inquiries. This is doubly so if you are looking for a personal loan with fair credit. Keeping the number of open loans down and keeping a minimum of loan and credit card applications out there will be to your advantage, regardless of credit score.

Conclusion

Finding the right loan for you can be a daunting task, especially if your credit is low. Do not try to go it alone. There are experts standing by to help you. Visit Loanry today to see what they can do for you!

Brandy Woodfolk is an educator, home business owner, project manager, and lifelong learner. After a less than stellar financial upbringing, Brandy dedicated her schooling and independent studies to financial literacy. She quickly became the go-to among family, friends, and acquaintances for everything finance. Her inner circle loves to joke that she is an expert at “budgeting to the penny”. Brandy dedicates a large portion of her time to teaching parents how to succeed financially without sacrificing time with their little ones. She also teaches classes to homeschooled teenagers about finances and other life skills they need to succeed as adults.

Brandy writes about smart money management and wealth building in simple and relatable ways so all who wish to can understand the world of finance.