Having good credit opens many doors of opportunity. Having less than perfect credit can cause you to do things the hard way, such as paying cash for your necessities or having to jump through hoops to get things done. It helps to understand how credit works. When it comes to credit, you need to understand terms, such as hard inquiry and a soft inquiry. What does that mean? What is the difference between hard and soft credit inquiry? How do these inquiries affect your credit? Is one inquiry worse than the other? Here’s what you need to know.

What Is a Hard Inquiry?

A hard inquiry occurs when a lender checks your credit. When you apply for a loan, the lender will check your credit, a hard inquiry, to determine your credit worthiness and financial responsibility before approving or denying your loan application. You need to use hard inquiries sparingly. A hard inquiry can remain on your credit for at least two years and can lower your credit score. Common loan applications that count as hard inquiries include

A hard inquiry occurs when a lender checks your credit. When you apply for a loan, the lender will check your credit, a hard inquiry, to determine your credit worthiness and financial responsibility before approving or denying your loan application. You need to use hard inquiries sparingly. A hard inquiry can remain on your credit for at least two years and can lower your credit score. Common loan applications that count as hard inquiries include

- Mortgages

- Auto loans

- Credit cards

- Student loans

- Personal loans

How Many Points Does a “Hard Pull“ Affect My Credit Score?

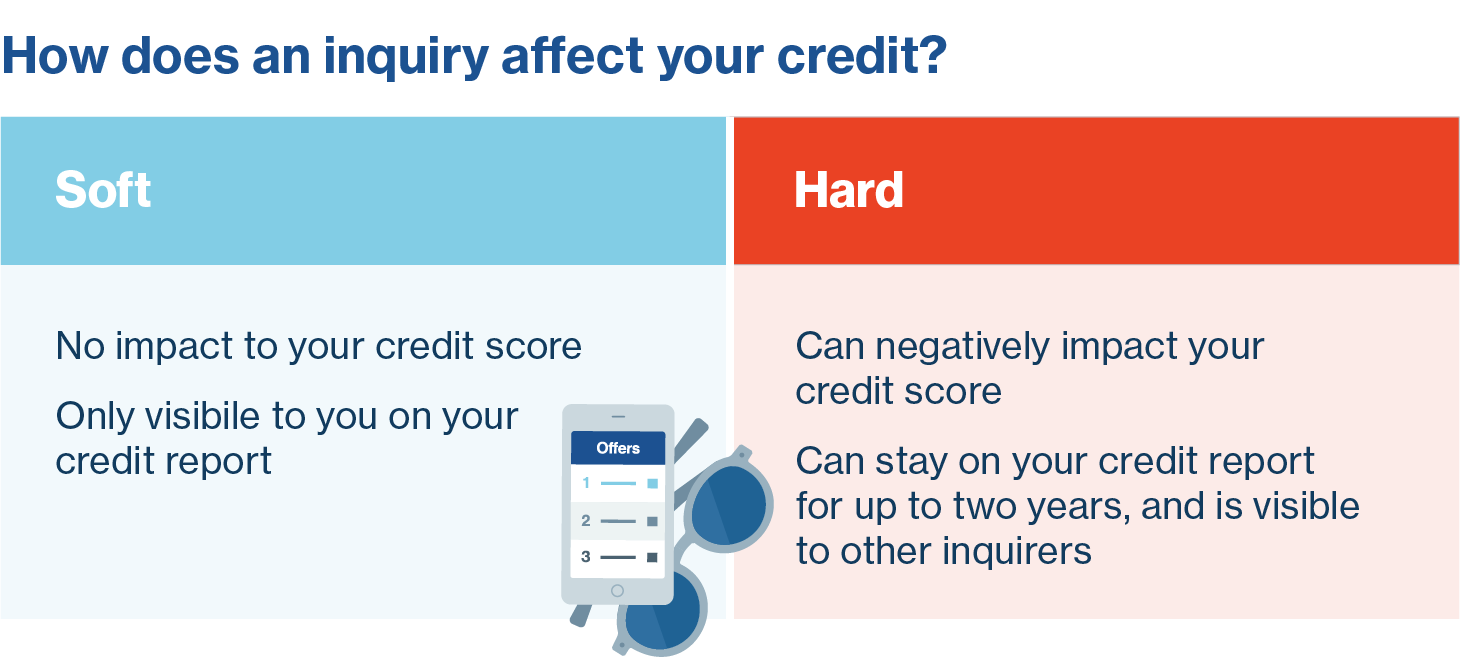

The effect a hard inquiry or a hard pull has on your credit score depends on your unique credit history. For many people, a hard credit inquiry affects your credit score by 5 points or less. Here’s what matters. If you have little to no credit or few accounts on your credit report, hard inquiries will have a much greater impact than someone who has an established credit history.

is the period that hard inquiries remain on your credit.

Having multiple hard inquiries on your credit makes you risk for lenders. That means lenders are less likely to approve you for a loan. If you have 6 or more hard inquiries on your credit, you could be at high risk for filing for bankruptcy. Hard credit inquiries are what lenders use to assess your financial risk before giving you a loan, but it does not play as much as a major role in defining your credit score as late payments and overall debt does.

What Is a Soft Inquiry?

A soft credit inquiry occurs when you or a company is checking your credit, often in the form of a background check. A soft inquiry could also be a mortgage lender pre-approving you for a loan. Did you know soft credit inquiries on your credit can occur without your knowledge and permission? Unlike hard inquiries on your credit, soft inquiries do not affect your credit score in any way. Common soft inquiries include

A soft credit inquiry occurs when you or a company is checking your credit, often in the form of a background check. A soft inquiry could also be a mortgage lender pre-approving you for a loan. Did you know soft credit inquiries on your credit can occur without your knowledge and permission? Unlike hard inquiries on your credit, soft inquiries do not affect your credit score in any way. Common soft inquiries include

- Viewing your credit on Creditry.com

- “Pre-qualified“ credit card offers

- Certain kinds of payday loans

- Employment verification/background check

Loans Without a Credit Check

If you’re getting a loan without a credit check, you still need to know the difference between hard and soft credit inquiry. Having little to no credit can be an issue in different situations, but getting a loan is not one of them. Yes! You can get a loan with no credit check.

Getting approved for a loan without a credit check is no walk in the park, but it is not impossible. Since getting approved for a conventional loan is out of the question right now, a personal loan is there to help. A personal loan gets you the money you need when you need it. While a personal loan may have higher interest rates accompanied by strict terms, getting a personal loan helps you cover unexpected expenses, such as emergencies. When emergencies occur, you don’t have time to wait on anyone or anything, and a personal loan gives you everything you need, so it’s worth taking a closer look.

Get Familiar With Your Credit Score

Although your goal is to get approved for a loan without lenders checking your credit, it’s always good to know where you stand. Some people check their credit and find their credit score qualifies them for a traditional loan.

Whether your credit score is fabulous or could use a little work, the bottom line is you need to know where you rank on the FICO chart with your credit score. Being knowledgeable of your credit helps when you need to approach a lender or bank directly. Now that you have an understanding, it’s time to approach the lenders directly.

Approaching Lenders Directly

Got jitters about approaching lenders? Approaching lenders could be in your best interest. Having a poor credit score or no credit at all limits your options for getting the cash you need. Dealing with lenders directly, even though you have less than perfect credit gives you other options to get approved, such as proof of employment and or income, which is used to determine your creditworthiness, since your credit score is not used as a determining factor.

The good news is more lenders are jumping on the bandwagon of using alternative data to determine a person’s financial worthiness. Alternative data lenders are using include personal information that is not found in your credit report, which is good. Why? Using alternative information improves your chances of being approved for a loan. When lenders look at your employment history or income instead of your credit score, more doors of opportunity open.

Getting Prepared

Having a solid work history and steady income is great, but you need to make sure you’re prepared. Creditworthiness is different when you’re trying to get approved for a loan without a credit check. Your creditworthiness in this situation is based on your education, income, employment history, credit card debt, bank statements, and more. The determining factor for getting approved for a loan without the hassle of a credit check is how well you can prove you are financially stable.

Stability can be proven by showing at least two years worth of tax returns or pay stubs for the last three or four months. If you currently have loans, such as student loans, auto loan or home mortgage, you can show that your payments are current and that you’ve made progress paying down the balance.

How Can You Find a Loan?

Are you interested in getting a loan? You can get a personal loan online, at credit unions, and at a bank. If you’re looking for a way to search and compare loans, getting a loan online is your best option. Getting a loan from your local credit union is a good option if you’re interested in having flexible loan terms.

If you’re feeling lucky, you can try to get a loan from the bank, but it’s important to check all of your available options before making your final decision and understand what happens before you get a personal loan.

Getting a Loan Online

Getting a loan online offers benefits such as convenience, easy access, saving time, and low rates. Before you apply, you need to become familiar with the difference between hard and soft credit inquiry. When you’re applying for a loan online, you have the opportunity to apply from the comfort of your home, and you don’t have to schedule an appointment or wait in line. As long as you have the information you need including,

- First and last name

- Home address

- Social security number

- Income/Proof of employment

Other information may be required, but that depends on the lender and their standards. When you’re filling out the form, it’s easy to miss a box that you need to fill. Make sure you fill each box because missing one can delay the receipt of your loan.

When you apply for a traditional loan, there are a lot of hoops you have to jump through and requirements that have to be met. A personal installment loan online requires less information to get approved and often has more flexible terms. Aside from these perks, the approval time is quick. It could take a few days, even weeks to get approved for a traditional loan, but when you apply for a loan online, you could get instant loan approval.

The longest time you would have to receive your funds when getting a loan could be three days, which is still less time than traditional loan offers. Along with quick and easy access, you can get a personal loan online even though you have less than perfect credit. Some of these online lenders can get you a personal loan as soon as tomorrow.

If you’re in a hurry and need money in a short amount of time, it’s in your best interest to apply for a personal loan. Traditional loans have to go through a lot of different paces before the loan is approved. If you’re pressed for time, a personal loan is your best option. In addition to quick approval time, there is not a lot of paperwork for you to fill out, which saves time.

You need to find a lender with the lowest rates, which means less money out-of-pocket for you. One of the greatest perks of getting a loan online is that you can compare rates and benefits of different lenders and choose which one suits your needs the best.

Getting a Loan from a Credit Union

Have you ever considered getting a loan from a credit union? A credit union is a non-profit cooperative, which is good news for you. Since credit unions are not-for-profit organizations, they’re more focused on helping you get what you need rather than their sole focus being maximizing profits, much like a bank. Even if you decide to get a loan from a credit union, you need to know the difference between hard and soft credit inquiry.

Credit unions are focused on the community, which often means they are local to a specific region or state. Speaking of community, credit unions work with each other. What does this mean for you? When credit unions work together, they are able to serve you better, which means you get what you need when you need it. Many of the services a credit union offers are more convenient than those of a bank.

Getting a loan from a credit union means you’re a member and not just your average customer. By becoming a member, you have access to better rates and lower fees. Due to the lower rates, you can earn a lot more money on deposits, and since credit unions give savings to their members, you have lower fees to pay. You can save money two ways with credit unions thanks to better rates and lower fees.

Getting a Loan from a Bank

Getting a personal loan from a bank comes with one or two perks and a lot of downfalls depending on the type of loan you choose. In this situation, you need to know the difference between hard and soft credit inquiry. There are two types of personal loans:

- secured loans and

- unsecured loans

Secured loans are ones that are made with collateral in place. If you don’t pay off your loan or miss payments, the bank can take your property as repayment for the loan.

If you decide to get a loan from a bank, your best bet is to get an unsecured loan. With an unsecured loan, you don’t have to worry about losing your assets, including your home. Being laid off or experiencing another financial hardship makes repaying your loan difficult or almost impossible to repay on time. If you get an unsecured loan, this means that even if you miss a payment or are late making a payment, you’re not at risk of losing everything you’ve worked hard to maintain.

In Conclusion

There is more than one way to get a loan. However, you have to decide which type of loan is best for your current situation. Having a less than perfect credit score makes getting a loan difficult, but not impossible. Weigh the pros and cons of each loan option before making your final decision. Make sure you understand the difference between hard and soft credit inquiry.

Finding a loan can be difficult and frustrating because there are many options. That’s where we come in and save the day. We will help you find and lender to get a loan that may suit your needs. Contact us today to see how we can help.

Blaine Koehn is a former small business manager, long-time educator, and seasoned consultant. He’s worked in both the public and private sectors while riding the ups-and-downs of self-employment and independent contracting for nearly two decades. His self-published resources have been utilized by thousands of educators as he’s shared his experiences and ideas in workshops across the Midwest. Blaine writes about money management and decision-making for those new to the world of finance or anyone simply sorting through their fiscal options in complicated times.