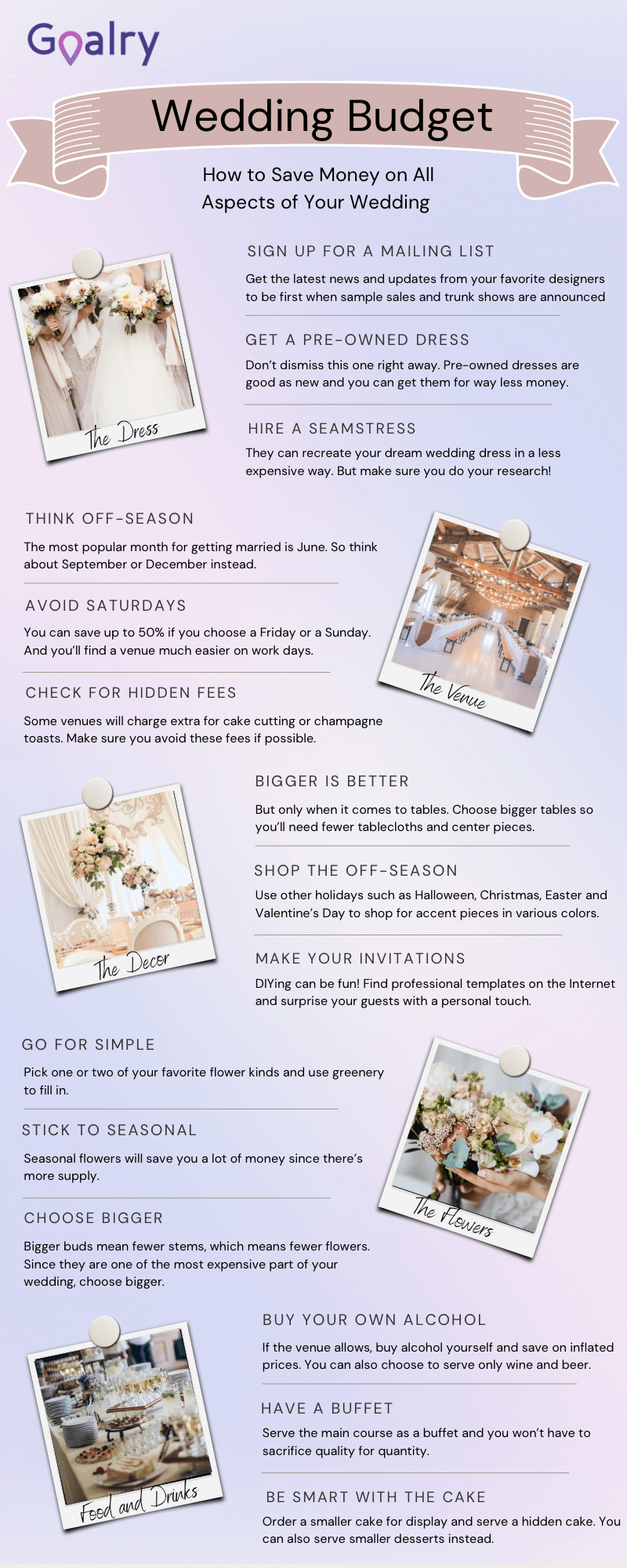

While weddings can be done at reasonable costs, many are extremely expensive. Since the day of marriage is one of the – if not THE – biggest days of your life, it’s no wonder that you want it to have all of the trappings. A great dress or suit, the perfect venue, top-tier decorations and catering…it all adds up to a significant sum. If long-distance travel is involved, costs go even higher. Because of this, it’s no wonder if you’ve considered taking out a loan for a wedding or for travel finance.

Before taking out any loan, you should always consider whether it’s a good idea in the long term. Many say that you actually should not get loans for wedding expenses. The Balance explains that the biggest issue of contention in a relationship is money, and that starting out your new life with a pile of debt can bring unnecessary friction. They suggest having a smaller wedding celebration and using the money that would have gone to loan payments for other options. The loan payment money could go to things like saving up for your first house, retirement, or investments.

What is a Wedding Loan?

In almost all cases, a wedding loan is just a personal loan that you’ve decided to use to pay for wedding expenses. It is unsecured, so you can’t lose your house if you don’t pay it back. Legally speaking, the term “wedding loan” is just a colloquialism.

As with other personal loans, your credit score is the main determining factor for approval. Your employment history will typically factor in, as well. If you’re unemployed, lenders are unlikely to be interested in financing your plans.

Should You Take Out a Personal Loan for Your Wedding?

Though some advisers are against the idea, others say that there are pros and cons to the idea of wedding finance. The goal is always to find ways to save money on your wedding rather then borrow it for the big day. Pros of taking out a loan for a wedding include:

- It’s easy to get a loan if you have a good credit score and stable income

- Interest rates are typically lower than that of credit cards

- It usually just takes a bit of paperwork to get the loan

- You’ll be able to pay for a bigger or more extravagant wedding

There are, however, some cons to keep in mind:

- It can be hard to start a marriage with more debt

- If you already have a lot of debt, the new payments can seriously pinch your finances

- Interest makes it so you have to pay back much more than you borrowed

- Those with bad credit will have to pay much more interest

Are Wedding Loans Worth It?

Only you know if taking out a loan for a wedding will be worth it. That’s because you know your finances, employment status, and your own tolerance to debt. For a wedding, be sure to talk to your partner as well. Even if you’re fine with the debt, there’ll be problems if he or she is against it.

With that in mind, the answer is, as they say, a definite maybe. If you’ve spent your life dreaming of a big, flashy wedding, you’ll be disappointed with a small one. You surely intend on your wedding to be a one-time event, so it can be worth it to make it extravagant.

On the other hand, if you loathe having to pay bills, it makes sense to avoid adding one to the pile. The same is true if you know that you’re likely to have periods of unemployment or underemployment. Then, it’ll be worth it to save up so you can avoid the stress.

Can You get a Personal Loan for an Engagement Ring?

Engagement rings are typically more affordable than wedding rings, but they can still be expensive. Because of this, the idea of taking out a loan for one may come to mind.

The short answer to this is “yes.” You can take out a personal loan for pretty much any legal purchase. As with a wedding loan, the approval will depend on your credit history and employment status.

Whether you should borrow money for an engagement ring depends on the same factors as taking out a loan for a wedding. It’s always a good idea to consider alternatives to loans. Note that you should also look for ways to keep the cost of your engagement ring down, such as shopping online.

Banks that Offer Wedding Loans

Since a wedding loan is a personal loan, you can get one at almost any full-service bank. Banks often do not advertise them as “wedding loans,” but if their underlying product is a personal loan with no real limitation on use, you can get one for your wedding.

According to Student Loan Hero, there are several online banks that can provide the needed funding. These include Prosper, Earnest, and LightStream. Loanry is another excellent source for all types of funding needs that include helping you find a lender.

Conclusion

Taking out a loan for a wedding is quite common, to the point that some financial institutions specifically list this purpose in their “reason for loan” drop-downs. As we have discussed, there are benefits and drawbacks to this solution. They can allow you to have a bigger or more extravagant wedding without the need to save up. On the other hand, they are debt, and debt of any sort involves interest and repayment.

Whether taking out a loan for a wedding is right for you depends on whether you are more attracted to the idea of the fancy wedding or to being debt-free. Think wisely before making your choice, and you should be satisfied with the results either way.

Cole is a personal finance research analyst and writer with extensive experience in building and maintaining a corporate brand utilizing both qualitative and quantitative methods. Cole has written on a diverse range of topics including financial planning, cryptocurrency, commercial real estate, and tax strategy. A graduate from Drexel University, Cole seeks to demystify financial borrowing and help individuals achieve financial freedom.