There have been a couple of times in my life that loan approvals and rejections have utterly shocked me. I have seen some people with really low credit scores get approved, and some with really high ones get rejected. It seemed so twisted, especially since I grew up hearing that your credit score was the “be all, end all” when it came to financial success. I realized very quickly that I had been given some bad information. Credit scores, it seems, are only a factor in the equation.

How Credit is Calculated

If your credit score is only a portion of the decision, what else is considered? Basically, anything that can show them whether you can repay. The bottom line with a consumer loan, or any other loan, is that the lender wants their money back, and they add certain things into the equation to determine if they will get it back or not. Your credit is not determined by a single item.

Instead, it is an equation of multiple factors- all of which speak to your ability and possibility of repaying the loan. These factors are lovingly referred to as the five C’s of Credit.

Understanding the Five C’s of Credit

Have you ever heard of the Five C’s of Credit? I like that name because it tends to lighten the seriousness- just a little bit. While credit is a serious thing, being way too serious and stressing out about it will only hurt you. Stress is a killer, so we are going to keep this on a less serious note as well. The five c’s of credit are going to help you understand credit terms and decisions a little better.

Imagine you are going on a trip to fabulous Honolulu, Hawaii. You want to take a friend along but cannot decide which friend to take. You want to be fair in your choice, so you decide to look at each friend objectively. Though you are paying for the trip up front, the friend you choose will have to pay you back and cover their own food. As there is money involved, you score each according to the following five categories:

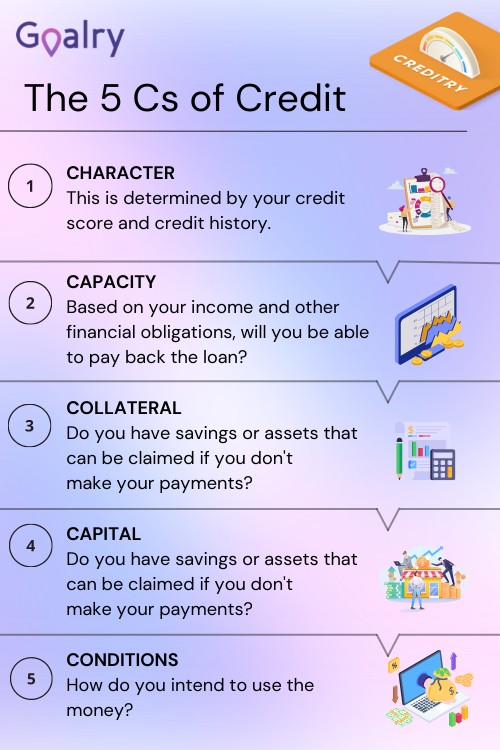

The Five C’s of Credit: Character

The first of the five c’s of credit is character- the one I happen to think is the absolute most important. A person’s character can lead one in the decisions he or she needs to make- like relationships or loaning money. In very simple terms, when it comes to the five c’s of credit, the character is based on credit history.

As far as your credit goes, your character is determined by your known previous financial actions– just as you scored your friends according to their known actions. The decisions you have made in the past speak to your character, to whether or not you are likely to repay the loan. In fact, whey judge your character by how likely it is you will be 90 days late or later in a two year period.

You may be saying, “But I’m in better financial shape now. It’s not fair that they judge how I will do now by what I did in the past. I was a stupid kid, then.” I know- I have had those same thoughts run through my head before, but you have to be fair to financial lenders, as well. They have no way of seeing the future, so they have to go by your previous actions.

It has often been said that past behavior is a predictor of future actions. How else can a lender decide if it is safe to loan money to you? However, while your character is a part of your credit worthiness, there are four other parts that are looked at. So while there is no guarantee, you might still have a shot at borrowing if the other factors look pretty good.

The Five C’s of Credit: Capacity

The second of the five c’s of credit is capacity. While character can be judged more subjectively, capacity is pretty straightforward. It is simply the ability one has to repay.

The second of the five c’s of credit is capacity. While character can be judged more subjectively, capacity is pretty straightforward. It is simply the ability one has to repay.

Lenders look at income capacity to see whether or not you have the ability to repay the loan. If your outgoing money is more than your income, they will say you do not have the capacity to afford a loan. And, truthfully, how comfortable would you be loaning someone money that did not have a way to repay you?

It would be better to just give them the cash and not expect it back. Though some friends may do that, do not expect a financial institution to. They want you to have an income that outweighs your ongoing debt.

The Five C’s of Credit: Capital

If one of the friends you are considering offers to put up half of the cost up front, you are probably most likely going to choose them- or at least move them to the top of the list. Why? Well, for one, they are easing your financial burden. If they put up half and you put up half, it is a lot less stress on you. Second, it shows that they really want to go and are serious about doing their part.

If one of the friends you are considering offers to put up half of the cost up front, you are probably most likely going to choose them- or at least move them to the top of the list. Why? Well, for one, they are easing your financial burden. If they put up half and you put up half, it is a lot less stress on you. Second, it shows that they really want to go and are serious about doing their part.

The same is true with lenders. When you apply for a mortgage loan, the lender usually wants you to pay a portion upfront. It could be as low as 2% and can go as high as the lender wants. The same is true with car loans- lenders want you to put up a down payment. And honestly, can you blame them? They are putting money towards something for you- something that may cost them a lot of money.

With you putting at least a portion of the cost down, it shows you are serious about this purchase. It means you have some skin in the game, so to speak. You have invested in it, so you are more likely to pay off the loan instead of losing your investment. It’s really that simple.

The Five C’s of Credit: Collateral

Capital is not the same as collateral, though they have been confused a bit. Remember that capital is your friend paying a portion of the cost up front. Collateral, on the other hand, is something your friend lets you hold until they repay you. It could be a piece of jewelry, a piece of stereo equipment, or something else that they find valuable. The agreement is that if they do not repay, you have the right to sell that collateral to make back your money.

Capital is not the same as collateral, though they have been confused a bit. Remember that capital is your friend paying a portion of the cost up front. Collateral, on the other hand, is something your friend lets you hold until they repay you. It could be a piece of jewelry, a piece of stereo equipment, or something else that they find valuable. The agreement is that if they do not repay, you have the right to sell that collateral to make back your money.

In the loan world, collateral may be a car title, a check, a piece of land, or anything else the lender finds valuable enough to regain their money. While collateral does not necessarily guarantee approval, it does improve your chances because a secured loan- a loan attached to collateral- is less of a financial risk for the lender. If you are applying for a loan, it might be wise to have something in mind that you can use as collateral just in case.

The Five C’s of Credit: Conditions

Conditions are just what it says- conditions surrounding the loan. That may seem pretty straightforward but there are many conditions that might affect approval.

Conditions are just what it says- conditions surrounding the loan. That may seem pretty straightforward but there are many conditions that might affect approval.

A lender has to consider all conditions. Of course. things such as the terms of the loan, i.e. principle and interest rates, need to be factored in. How else will you or the lender know if you can afford the loan? However, there are other factors that are beyond the borrowers’ control that still have to be considered- such as the housing market, in general. A borrower has no control over the condition of the housing market but it can prevent loan approval.

The Equation

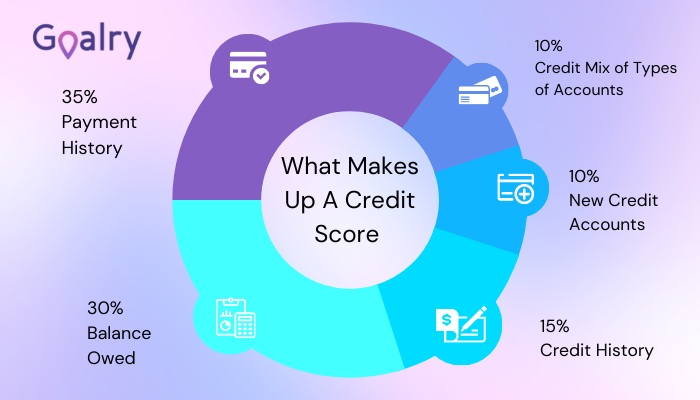

While numbers themselves might be absolute, the ways they are calculated can change quickly. Those five c’s of credit we just discussed are all consistent factors of the equation, but the level of importance of each of them can change from lender to lender and loan to loan. Here is the thing many people I know do not pay attention to: your credit score is not all that lenders look at. And, for that matter, your credit score is not just figured according to how much you owe or how much you have paid off. It is based on a mixture of things.

When lenders check your credit report, they will be looking at all of the factors, but the weight of those factors will be different. While one lender may place more importance on character another may consider capacity more important. With secured loans, collateral is often the most important factor. With home and car loans, capital is probably going to rank higher. There are some lenders that only factor in your capacity and, possibly, your collateral.

Finding a Lender

The bottom line with this is that there is no concrete equation that you can plug everything into so you will know if you can get approved. Most lenders will have their own equation, so you will only know for sure when you apply. And since the equations differ among lenders, just because one says, “No”, does not mean they all will.

So if it is so different among lenders, how do you know where to get a loan? You will have to credit shop. This means searching for the type of loan, rates and terms you want among multiple lenders. Then, you apply at each of them because that increases your chances of finding a lender to approve you.

Yes, I know- it sounds time-consuming. It can be but it does not have to. That is why places like Loanry exist. We help you find a lender. You simply fill out your information, and we find a lender that may fit your situation. If a lender wants more information, they will ask you for it, but you are not wasting time applying for loans that are not even in reach. It simplifies the process completely.

What To Do If You Do Not Get A Loan

If you have exhausted your lending options, cannot find a loan that meets the terms you want, or you are through looking for some other reason, you have two options: give up completely or make yourself a more desirable borrower for the future. Though it can take time, persistence, and a strong will, you can improve your overall credit and increase your odds of approval by using the five c’s of credit to do so. Just follow these steps:

Remember, character is about your credit history, so to build your character you have to improve your credit history. How can you get credit to improve your credit if you cannot get credit? That’s a great question. Perhaps you could not get credit in the ways you were trying to, but there is something else you can do.

Go to your local bank or credit union and deposit some cash into an account- probably around $500. Don’t freak out yet by saying you do not have $500 to spare because you do not need it to spare. Go to the loan office of that credit union or bank and apply for a secured loan using the cash you put in the account as collateral.

Explain that you are looking to rebuild your credit and you would like to start with this secured loan. Most likely you will be approved because they will usually approve you for the same amount that you have deposited. Again, there are no guarantees, but it is very likely.

This type of loan is good for you because you get the same amount you deposited- meaning you are not losing money, and neither is the bank if you decide not to pay. If they did not approve you for some reason, you can just withdraw your money. Easy as pie.

If you are approved, though, you can begin to rebuild your credit. Make timely payments each time so good marks go on your credit report. For those that can spare any of the loan, put it away to use for payments. Make each payment to the best of your ability. Once it is paid off, do it again and again until you no longer need collateral.

Again, your capacity is determined by your income versus your consistent outgoing funds. The goal is for the incoming to exceed the outgoing. To do this, pay off any bills that you can, renegotiate things like your cable, and any other item you pay that could be gone or at least decreased. At the same time, increase your income. Ask for a raise, apply for a promotion or a new job altogether, or pick up a second job.

If you want to purchase a house, or other large purchase, you need some capital. The amount of capital lenders want fluctuates according to the market and other conditions, so it is hard to put a dollar amount on how much capital to have. However, determine a goal according to the current rates, and once you find or make that amount, apply for something that fits with that.

For instance, let’s say you are aiming for a $100,000 house and lenders are currently looking for 10% capital. This means you need $10,000. When you have that amount together, you find that they are now looking for 20% capital. You have three choices:

- Wait to see if the amount goes back down

- Find the other $10,000

- Find a home for $50,000 so you already have the capital ready

Obviously, that choice is yours. If you are looking for the home you plan to stay in for the next 50 years, you probably do not want to compromise on the type of house you buy. On the other hand, if you are moving to a different state because of a new job that will only last a few years, you could be more flexible.

Having some collateral to put up will generally increase your chances of approval, though it is not a decision to take lightly. Understand that collateral means the lender can take that property and sell it as a means to recoup their losses. While I sincerely hope that you have no intention of defaulting on a loan, life does happen, so you need to be mindful of the collateral you use. You should choose collateral that will not throw a huge wrench in your life if you lose it.

Let me put it like this: collateral needs to have some value or it is of no use as collateral. A car is valuable monetarily, but it is also valuable as your vehicle. It is most likely what gets you and your family back and forth to where you all need to go. So, before putting it up as collateral, really think about it.

Do you have another vehicle you can use? If not, can you easily walk back and forth to work or take public transportation? Basically, can you continue the things you need to do without that vehicle?

Lenders may require a certain type of collateral, so you may only have the choice between using your car title or not getting the loan. If that is the case, you must simply decide if it is worth the risk. Collateral may improve your odds of getting the loan, but you do not need it hurting you in other ways.

If you are unsure of why you are not getting approved, there are ways to find out. First, when you apply and are denied, the lender is supposed to send you a letter in the mail explaining why. It might say things like, “Too many delinquent accounts”, “Judgment including bankruptcies”, “Not enough open accounts”, or something totally different. You can use these notes as a starting point.

Additionally, you can obtain your credit report for free. Once a year, you can get a free copy through each credit bureau: TransUnion, Experian, and Equifax. You want to get a copy from all three because there tends to be different things on each. To get a comprehensive view of which of the five c’s of credit need the most work, you need to see what all you are fighting against.

Also, when you get denied for credit, you have a certain amount of time to request a free copy of your report. The letter that you received from the lender will give you the information to do that. These are just two ways to keep an eye on your credit.

There are a few things that I do to keep a constant eye on mine. I am signed up with Credit Karma and CreditWise through Capital One. I love both because they alert me when something changes for better or worse on my credit. This is great because if something is not right, like a charge I did not make, I know pretty quickly and can take care of it. I also love them because they break down my credit and give me suggestions for improvement.

How to Evaluate Your Credit

No matter how you do it, it is important to keep an eye on your credit, and to consistently evaluate it against the five c’s of credit. The quicker you know these things, the better. To lighten the burden, though, when I say consistently check your credit and evaluate it, I do not mean daily- or even weekly. The first time you look at it, it will take a little bit. Be prepared to spend some time really working through your credit reports. After that first time, though, once a month or so should be enough.

Pick the first three debts you wish to pay off. I know a lot of people say to list them all at once, but I tend to find myself irritated when I do this. For one thing, the list looks like a mountain I cannot climb. Second, credit changes consistently. If I go through the trouble of listing them in order just to have to change it next month, I am probably not going to continue. Building credit is tiring enough without adding extra work. So pick three and start working. Pluck at it as much as you can- even if it’s $5 a month. It will add up.

Lastly, look at your credit report with fresh eyes. Pretend you are the lender. Would you loan to this person? If not, why not? Which of the five c’s of credit need to be worked on the most? What could the borrower do to change your mind over time? Make a list of those things and turn all of this information into a strategy that you can follow.

Conclusion

Whether you are looking for a loan or building your credit, you just might need to be a bulldog. Have your goal in mind and push toward it until you reach it. For assistance shopping for cash loans, Loanry is standing by to help you find a lender that may suit your need. For assistance building your credit, enlist a trusted friend to push you when you feel like giving up. No matter your goal, you can reach it if you are ready to fight for it.

Brandy Woodfolk is an educator, home business owner, project manager, and lifelong learner. After a less than stellar financial upbringing, Brandy dedicated her schooling and independent studies to financial literacy. She quickly became the go-to among family, friends, and acquaintances for everything finance. Her inner circle loves to joke that she is an expert at “budgeting to the penny”. Brandy dedicates a large portion of her time to teaching parents how to succeed financially without sacrificing time with their little ones. She also teaches classes to homeschooled teenagers about finances and other life skills they need to succeed as adults.

Brandy writes about smart money management and wealth building in simple and relatable ways so all who wish to can understand the world of finance.