Let us face it, most of us need a loan at some point in our lives. Unless you are independently wealthy, you are going to find a time when you need a loan. Most of us cannot, or choose not to, put out a large sum of money for large purchases, such as a car or house. You may even need a loan for smaller purchases.

Or, you may find yourself in a position where an emergency arises and you need money fast. Those are times when you may need a consumer loan. I understand that the thought of a personal loan may be a scary one. We are going to make the process less scary with this guide. We are going to share many tips, including where to get a loan.

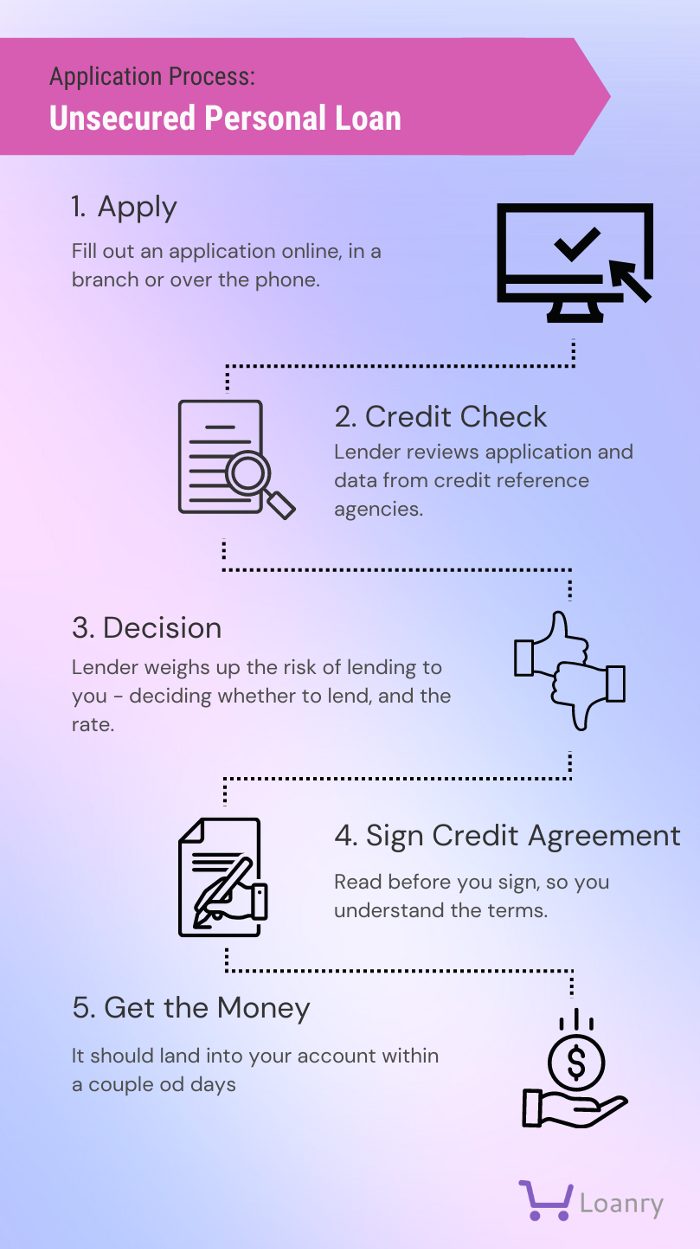

Personal Loan Process – Step by Step

The amount of money you pay per month depends on how much you borrowed, the length of time and the interest. We will talk more about interest a little bit later. A personal loan can be used for just about anything. The lender typically asks you what you plan to do with the money, but they do not use that reason as a determining factor.

Step 1. Apply For A Personal Loan?

You have decided that you want to get a personal loan, but you do not know where to start. You know you need to do some loan shopping to find the right one for you. The easiest part of the loan process is the application process. Depending upon on what type of lender you choose, the application process make vary slightly. The easiest of all applications is an online loan.

You simply fill out the online application and submit it. After that submission, the lender determines what documentation is needed. You must then submit those documents online. If you pick a more traditional lender, you have to go into the bank and fill out the application.

At a traditional bank, they have representatives that help you fill out your loan paperwork. When using an online lender, you have to fill out all the paperwork on your own. It is really a simple part of the personal loan process. It may take you more time to collect the documents for the bank than it does to fill out the application.

What Documents Do I Need for a Personal Loan?

As I stated above, the application process is fairly simple. There is always documentation that the lender asks of you. The first thing you need to provide is proof of identity.

This should be something that has your picture and name on it, such as a drivers license, military ID, or passport. You also need to provide proof of income. You can do this with paystubs, W 2 forms, tax forms and documents, and bank statements.

The lender may ask you to provide proof of your rent or mortgage payment and your utility bills. You should expect to provide any of this documentation within a few days notice. The lender may also ask you for proof of any retirement or annuity payouts you might be getting. You can always ask why they need the documents, but keep in mind, failure to provide them may mean you are denied.

Step 2. Credit Check

You may think that your credit score should not be a big deal, but lenders think it is. Your credit score is a large part of the personal loan process decision. So, let us spend a few minutes on credit scores. Your credit score is a three digit number that could stand between you and a new house, or car. It can, in some instances, even prevent you from getting a job. So, it’s really important and you should understand why.

It may seem like only a number to you, but to a lender it signifies how risky you are when it comes to loaning money. Credit scores range from 300 to 850. The lower your credit score, the worse your credit is considered. Anything above 700 is considered a good score. Anything below about 650 is starting to get into the fair to bad range. Most people fall into the 600 to 750 range. The reason for most credit scores dropping is late or missed payments. It is hard to get and maintain a good credit score.

It only takes one or two mistakes and your credit score decreases. If your credit score is low, you can bring it back up but it does take consistent and hard work. You should protect your credit score and do everything you can to not let it fall below what is considered good.

What if I Have Bad Credit?

If you do not know what credit score you have, you should pull your credit report and take a look at it. You want to make sure there are not any errors on your credit report. If there are errors, you should work to get them fixed. If you can fix some of the errors on your credit report, you should be able to improve your credit score. Once you know what is on your credit report, you can decide how to handle it.

If you do have bad credit, you can still get a loan. It may be a little harder and requires more work on your part, but it is possible. When you have bad credit, some banks will not approve you for a loan. Other lenders, like credit unions and online lenders, are more willing to loan you money with bad credit. The interest rate is going to be higher, so you end up borrowing more money.

The lender may require that you have collateral. A loan with collateral is a secured loan and it means that you are using something, such as a car, house, or jewelry to secure your loan. If you do not pay back the loan, or default, the lender can take your collateral and own it.

The good news is the lender gives you one last chance to bring the loan current so you do not lose your collateral. If you do not have the best credit, you need to shop around to find the best loan for you. Most importantly, read all the fine print and understand the personal loan process.

Step 3. Lender Decision

Once you apply, the lender sends your application to the underwriter. This is part of the personal loan process where you just have to wait. You do not have anything to do during this time. It can also be the most frustrating part of the process because you truly have no control. You just wait and see what happens. You may be asked for more information during this process, so be prepared.

During this time, the underwriter looks at all of the documentation you provided, checks it and double-checks it. The underwriter looks over your credit report, reviews your income and debts and does some other administrative tasks. If your loan is approved, the rest of the documents are filled out and sent back to the lender. The lender contacts you and lets you know it has been approved or denied.

This is when you confirm the amount for which you are approved. The terms of the loan are outlined for you, including the interest, your monthly payment and how many months you must pay back the loan. Up until this point, all of the numbers are tentative and considered subject to approval.

What Do Lenders Look At When Approving A Personal Loan?

Lenders look at different pieces of information when determining approval for a loan. Income and credit score are two of the major factors a lender uses to determine approval. Let us table credit score for just a moment and focus on income and some of the other factors. Most lenders want you to have a job, or a steady stream of income.

There are title loans that depend solely on the title of a vehicle, but we are not considering that type of loan in this situation. Lenders want to verify your employment. They ask for paystubs and bank statements. They may even want to call your employer. Not only are they interested in how much money you make, but how long you have been with your employer.

Lenders determine your stability based on how long you have stayed at one job. If you bounce from job to job, they may think you are not stable and therefore a risk for lending money. They also want to have faith that you can pay back your loan. A stable income indicates that you should be able to repay. The more money you want to borrow, the higher the lender wants your income to be.

Step 4. Sign Credit Agreement

One of the most important pieces of your loan is the interest rate. As I mentioned before, the lower your credit score, the higher the interest will be. Ultimately, that means you borrow more money.

Lenders use your credit to determine the annual percentage rate (APR). Interest rates can vary anywhere from 5 percent to 36 percent. Those with the best credit get loans with an interest rate of 5 percent. Those will poor credit end up with 36 percent interest.

The best way to illustrate this is with an example using numbers. If you plan to borrow $10,000 and have 5 percent interest, that means your total interest is $500. You borrow $10,500 from the lender. If the term of your loan is 36 months, that means you will pay $291.67 per month.

Now, let me show you how that changes at 30 percent interest. You borrow $10,000 at 30 percent interest, which makes your total interest $3,000. The total amount you have borrowed from the lender is $13,000. Your monthly payment becomes $361.11.

With a higher percentage rate, you end up borrowing $2,500 more and pay about $70 per month. I have shown you two extremes here to really emphasize my point. You should shop around for the best rate for you by spending the time to look for the right lender for you. This helps you save money in the long run.

Are There Fees With A Personal Loan?

When you are looking for a personal loan, always look at the fine print. Personal loans may have fees associated with them. They are part of the personal loan process and it is important to know about them ahead of time.

Some of the fees of which you should be aware are origination fees. An origination fee covers the administrative costs associated with the loan. It covers all the paperwork that occurs. The origination fee is rolled into the loan payment.

A lender may charge an application fee. This is a fee simply for you to fill out the application. This is a fee that you must pay out of pocket before the loan is even processed. If your loan is denied, you still have to pay the application fee. All other fees are charged as part of an approved loan. If your lender is charging you an application fee, you may want to find a different one. There are many lenders that do not charge this fee.

There is a late payment fee. This is typical for most bills. If you pay the bill late, there is a fee you will pay. The fee varies with each lender, so be sure to read the contract. You also want to determine if the fee increases with each subsequent late payment. In addition, when you make a late payment, it can have an impact on your credit.

Another fee your lender might have is an early payment fee. Sometimes, this may be called an early termination fee. The lender may charge you this when you pay back all the money you borrowed early. The bank makes money off of you by charging you interest. When you pay off the loan early, they lose the interest on that additional time. They may charge a fee to offset the money they are losing. You must be sure that you understand all of the fee associate with the personal loan process of the loan for which you apply.

Step 5. Get the Money

The amount of money received can range anywhere from $200 to $100,000 depending on your credit, the lender’s loan amounts, the amount you request and more. Money can show up in your account as soon as tomorrow.

Is A Personal Loan Right For Me?

Ultimately, you are the only person that can answer that question. You must decide for yourself if you should apply for a personal loan. However, there are some factors that can assist you in making that decision. First, do you really need one and can a personal loan fit within your budget. What is your intention for the loan and is it something you really need? You should also ask yourself, does a loan payment fit into your budget.

In other words, can you afford to pay it back? You really must take a hard look at your budget. Remember, while it is nice to get a large sum of money, you always have to pay it back. Once you use that money for something else, you still have to make monthly payments. The first step is understanding your budget. You should know how much money is coming into your bank account. You also should know how much is going out of it. Then look at what is left. If it is zero, or close to it, a personal loan may not be for you.

Which Lender Is Right For Me?

There are so many lenders on the market willing to lend money. You get emails offering you special rates. You still get mail in your mailbox with all of their special offers. Perhaps, you’ve even seen commercials on TV. But how do you know which one is right for you? There is no magic involved. The right lender for you is the one that gives you the best deal and fits your parameters.

The lender that gives you the money you want to borrow with terms that are agreeable to you. A lender that makes sure you are comfortable with the personal loan process is the right one for you. Make sure whichever lender you pick, it is a credible one. Make sure you understand all the fine print and the lender is willing to answer all of your questions.

It’s important that the lender you’ve choose is reliable and serious. Don’t just go with the first lender you find. Do your research and pick the best option.

Should I Consider An Online Loan?

I am sure that you have heard of cash loans online. You may have heard something like get money fast. Or even, fast cash in your bank account. While those are typically presented by online lenders, not all online lenders are alike. Online loans are on the rise as one of the top ways to apply for a loan. The process is super simple:

You fill out a quick application online from the comfort of your home. Then you supply the necessary documents by uploading them online. You usually get an approval within 24 hours of completing the application. Then the money is in your bank account within 24 hour of the approval. It really is the simplest personal loan process you can do. Do not get too excited, yet. Online lenders can be great. There are a few things to keep in mind.

One is that you can often receive a higher interest rate from an online lender. This is not a hard and fast rule, but there is a high chance. Pay attention to the bottom line. Look at the interest rate and make sure it works for you. Do not get sucked in by how fast and easy it is. Fast and easy might cost you more in the long run. Just pay attention and know what you are signing.

Applying with an online lender can be more risky. There are many people out there looking to scam people out of money. These people prey on those in desperate situations. Someone looking for an online loan might be desperate and might not be as vigilant as he might be in a different situation. Scammers now this and look for easy targets. Do not be an easy target. Always do your research.

Always find out information about a potential lender. Lenders must be authorized to do business in your state. Make sure the lender has proper certification. Make sure that you can find information about the lender and do your research. Spending a few hours researching a lender can say you a lot of headache and lost money in the long run. Your financial security is worth the extra time. As always, read the fine print and understand the terms of any contract you sign.

Conclusion

We have gotten to the end of the guide to understanding the personal loan process. We hope that you have a better understanding of the entire personal loan process. There are some key points that we really want you to take away from this guide. You must know that your credit score matters and can make a huge impact on your loan and how much money you end up paying.

You need to understand how your credit score is calculated and what impacts it. It is important that you read the find print of any loan application that you sign. Make sure you are getting the best loan for you with the best rate. Most importantly, you need to make sure you can afford to pay back the loan. You need to take a hard look at your budget and determine if you can actually afford to pay back the loan.

Remember, protecting your credit is the most important thing you can do. You do not want to do something that hurts your credit.

Julia Peoples is a long-time business manager focused on providing decision making assistance to the public. She works with people at key points of their lives who are making important retirement and financial decisions. She has had many articles published that educate the public on sound financial decision making.

Julia writes for those who are working towards financial freedom or a better understanding of how finances work. She has shared her financial insights with individuals on a one on one basis for years.