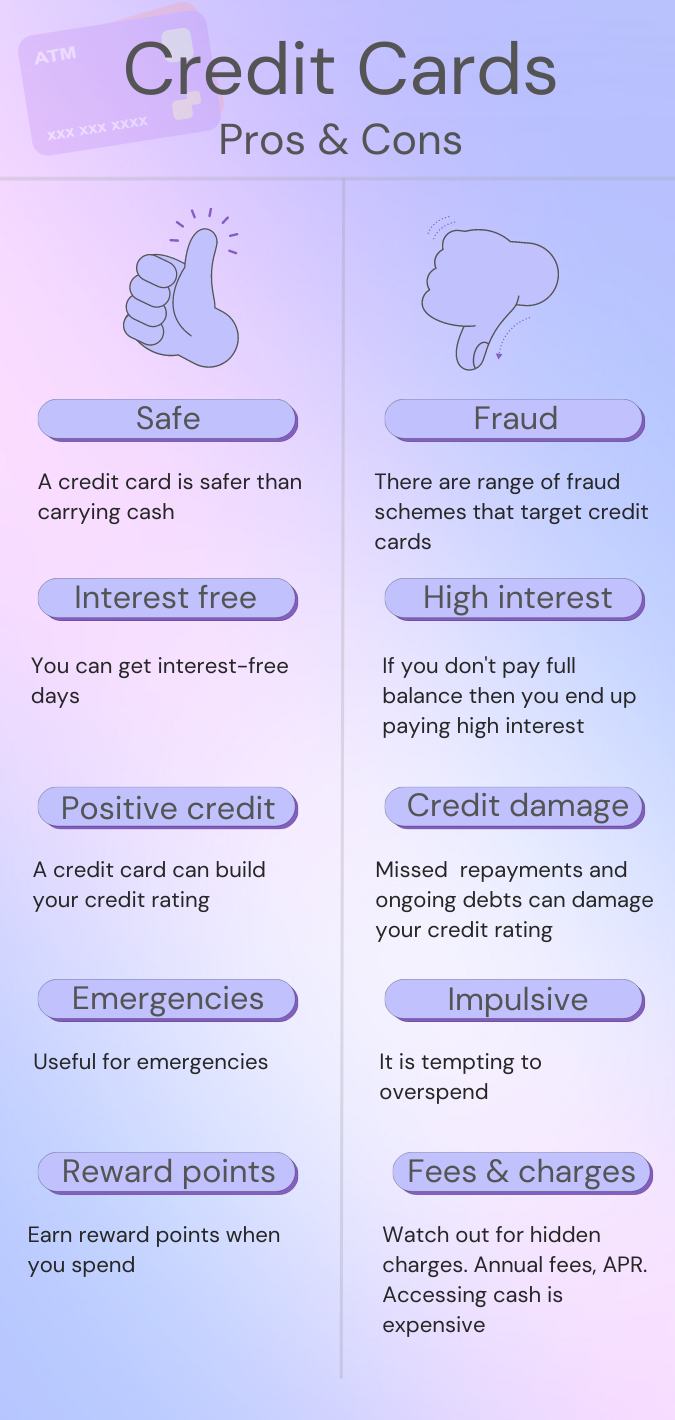

Having a credit card is important to financial independence and security. However, if you want to credit card to work for you and not against you, you have to use it wisely. The first step is making sure that you choose the right credit card for you and your needs. Once you have researched all the credit card options, you can select the one that is right for you. Even when you select the best one for you, you must use your credit card wisely so that you do not find yourself buried in debt.

Rotating Credit Card Categories Explained

A number of credit cards offer rewards when you make purchases in certain categories, or at specific retailers. There can be different types of cash back rewards with different types of credit card options. Some of them are fixed, while others have rotating credit card bonus categories. One type of cash back is a flat cash back rate on all purchases and there is not limit to the rewards. Another type of cash back reward is a tiered program. In a tiered program, some purchases earn more cash back than others. These tiers usually remain the same and do not change. The third category is a rotating bonus, which we will talk about a little further down.

With the cash back rewards that do not rotate, the rewards rate remains the same all year long. These cards offer unlimited cash back, which means there is no limit on how much you can earn in rewards. You can earn rewards on every purchase you make regardless of the amount you spend. A card with tired rewards usually breaks down so that you get 3 percent on groceries, 2 percent on gas, and 1 percent on every other purchase.

What Are Rotating Bonus Categories?

The third category we mentioned above is rotating credit card bonus categories. This is when a credit card offers different cash rewards on a quarterly basis. These cash back rewards are usually 5 percent on the amount you spend in specific categories or with a specific retailer. There is usually a flat reward amount for all other spending. Some example of categories may be grocery stores or gas stations, or it might be a specific retailer like Amazon.

These bonuses are typically a little higher and only last for a quarter, which is 3 months. Sometimes, the credit card will give you a heads up about which category or vendor is coming in the next quarter. If you plan to make a large purchase in this category, you might want to wait until the next bonus quarter.

What Are Some Common Bonus Categories?

When looking for rotating credit card bonus categories, you will find that each of these credit cards offers something slightly different than the other. They may rotate through the categories differently, but you will most likely find that they have similar categories.

Most of these types of credit cards have gas stations, grocery stores, and restaurants at some point in their rotation. You can usually find their scheduled rotation somewhere in the information about the card. If you find that you go to the gas station more in the summer, you might want to find a card that offers bonus cash back during the summer months.

You will also find cards that offer cash back for Amazon, Walmart, Home Depot, and Walgreens on their lists. You may even be able to find cards that offer rotating bonus categories on gym memberships and PayPal. Some newer categories include streaming services. Some cards may have an overarching category of streaming services, while some may specifically state Hulu or Netflix.

Is There A Downside To Rotating Categories?

When looking for rotating credit card bonus categories, you may want to know if there are any downsides to this type of credit credit. It is easy to see the high percentage cash back and be pulled in. If the credit card you pick requires you to activate your cash back savings, then it is on you to take that step. Your credit card company may or may not remind you of the new categories and that it is time to sign up. Another potential down side is if thee quarterly cash back options are not in alignment with your spending habits, it may not be the right fit for you.

The categories may not be in an area where you spend money or perhaps the timing does not line up. If you spend more money on gas in the summer months, but the credit card offers cash back bonus for gas in January, that may not be the right match for you. One more thing to consider is the potential cap on spending. If you are spending money that you might not spend just to get the bonus but you have reached your spending limit, you may be spending money for no reason.

What Are the Perks of Having a Cash Back Credit Card?

There are some benefits to having a cash back credit card. The money you get back is a percentage of your purchase. That translates into cash. You usually have the choice of getting a check mailed to you, money deposited into your bank account, or you can use the cash back to make a payment on your credit card. If you use your credit card for all purchases it can be a substantial amount of money. When you have a card with rotating credit card bonus categories, you can maximize on the amount of money you get back.

We will show you with numbers how cash back will work.

If you have credit card that gives you 3 percent back on all purchases, it could work this way: If you spend $1,000 per month, 3 percent of $1,000 is $30. If you spend $1,000 per month for an entire year, you can earn $10 each month, which is $120 per year cash back for purchases you were planning to make anyway.

What Cards Have High Credit Card Rewards Rate?

When considering rotating credit card bonus categories, it is helpful if you know which cards offer the highest rewards rate. You might want to start with these cards and create your list from there. Chase and Discover offer 5 percent cash back on specific categories each quarter. They do have a cap of $1,500 spending per quarter. That means that you receive the 3 percent cash back only up to $1,500 of purchases per quarter. If you spend more than $1,500, you will not receive cash back on that additional amount. In addition, they offer 1 percent cash coach in all other categories. You do have to activate the rewards each quarter. It is not automatic.

Citi cards offers a similar card called the Citi Dividend Card. This one is not available to new applicants. This card pays 5 percent back on items in specific categories and 1 percent back on all other items. There is not limit on how much you can spend, but the maximum cash back you can receive per year is $300. The Amalgamated Bank of Chicago (ABOC) gives 5 points per dollar spent up to $1,500 in specific categories, which change every quarter. The rest of your spending gets 1 point per dollar. There is no activation required to gain access to the cash back.

How Do I Pick The Right Card?

Understanding the cash back that comes with your credit card is important, but that is not the only reason to select a credit card. There are some other details to which you should pay attention. You should know the credit limit that comes with the credit card you are researching. The credit limit may make a difference depending on what your credit card needs are. If you want to make large purchases, you will want a credit card with a higher credit limit. You want to know the fee schedule for your credit card.

Most credit cards have late fees or missed payment fees. You want to know what those fees will be. You want to do everything you can to make sure you pay your credit card in full and on time, but things happen and you will want to know the fees associated with missed payments. The annual percentage rate (APR) is also important when selecting a credit card. This is the amount of interest you will pay if you do not pay your card in full each month. The higher the APR, the more interest you will pay each month. While your goal should always be to pay your credit card in full each month, we know that is not always possible. You should aim for the lowest percentage rate possible.

What Other Benefits Can a Credit Card Offer?

There are other bonuses that your credit card may offer. It depends on the credit card that indicates the bonuses you might get. If it is a store credit card, you often get special sales and incentives. You may also get loyalty points when you shop in the store and use the credit card. Some cards offer airline points. Every time you use your credit card, you get points for each dollar you spend and those points translate to savings on airline tickets. This credit card may also offer you travel insurance or protection on your purchases. Some credit cards offer gift cards as a reward for your purchases. You may even get gifts that are offered based on how much money you spend.

How Do I Use A Credit Card Wisely?

No matter what credit card you choose, you should always use your credit card wisely. If you are able to go to online card shops or go to stores in person to shop, you still should not spend more money than you have. It is easy to spend the money since it does not come directly from your bank account. You still have to pay the credit card bill each month. You should pay the credit card bill in full each month. If you cannot pay the bill in full, you should pay as much of it as you can.

When you accrue interest each month, it becomes harder to pay your credit card bill. This is how people get buried in credit card debt. Even if you cannot pay your credit card bill in full, you want to make sure that you pay at least the minimum amount and pay it on time. If you do not pay the minimum, you will be charged a fee. You want to avoid fees as much as possible. If you do not pay your credit card on time, it can have a negative impact on your credit score.

Conclusion

Picking a credit card is an important choice. It is easy to be lured in by the perks and cash back programs. You also want to make sure you pay attention to the credit limit and the annual percentage rate. You want to make sure that you selecting the best credit card for you. If you plan to use it often, you want to make sure that it is a perfect fit. You want to always remember to spend wisely. Just because you have the credit card does not mean you should always use it. You still must be mindful that you can pay your bill each month.

Julia Peoples is a long-time business manager focused on providing decision making assistance to the public. She works with people at key points of their lives who are making important retirement and financial decisions. She has had many articles published that educate the public on sound financial decision making.

Julia writes for those who are working towards financial freedom or a better understanding of how finances work. She has shared her financial insights with individuals on a one on one basis for years.